I can understand these fears, but I think there are still some positives to this story. The company's NFC business appears to be doing pretty well, and the higher-margin broadband and networking businesses are likewise more than just afterthoughts. I'd be nervous making a long-term commitment to any mobile chip company right now, but Broadcom could work as a rebound trade for aggressive investors.

Q2's Results Weren't That Bad...

Broadcom reported revenue growth of 6% (year-on-year) and 4% (sequential) for the June quarter, slightly below the average sell-side estimate. While broadband (up 5% and 6%) and infrastructure (up 7% and 19%) were stronger than expected, the mobile/wireless business (up 7% and down 3%) was almost 10% below expectations.

While the growth (or lack thereof) of the mobile business pretty much dominates the discussion around Broadcom, the company's other units are actually more profitable, and the company benefited from that mix shift. Gross margin declined 40bp from last year and rose 20bp sequentially. Operating income was up 3% and 10%, though, which was slightly better than expected despite very weak margins in the wireless business.

SEE: Analyzing Operating Margins

… But Guidance Was That Bad

Broadcom shares almost certainly weren't going to outperform on the basis of the reported results, but management's guidance and comments on the call seriously spooked the market. Management gave a range of revenue estimates for the third quarter with the midpoint about 5% below the prior sell-side estimate. Even worse, they pushed back the commercialization target for the LTE products by about six months – a significant delay in what many analysts have marked as a key driver of the company's near-term growth prospects.

What's Really Going On With Sockets And Shares?

A lot has been made of Broadcom losing connectivity slots in recent Samsung devices to Qualcomm as proof that Broadcom's mobile business is about to face serious trouble. To be sure, I do see some risk that Samsung shifts more business to Qualcomm or Marvell (Nasdaq: MRVL) in the future and/or leverages its purchase of assets from CSR to cut Broadcom out of future designs. Likewise, the announcement of Texas Instruments (NYSE: TXN) selling its connectivity assets to an unnamed buyer (speculation has centered on Apple (Nasdaq: AAPL)) has bears projecting significant share, ASP, and margin losses into the future.

That may be premature. It is true that Qualcomm has been winning sockets that were formerly Broadcom's, but it's also true that Broadcom has been winning baseband business elsewhere and this can actually be more lucrative. What's more, Broadcom has been beating NXP Semiconductors (Nasdaq: NXPI) and gaining some share in the NFC chip market.

It's also worth noting that Broadcom's non-mobile/wireless businesses aren't exactly chopped liver. Although the company wrote down the NetLogic deal by $501 million, the new Trident II networking chip is ramping with customers like Cisco (Nasdaq: CSCO) and Huawei, and these business can still drive worthwhile higher-margin growth.

The Bottom Line

At today's price, I think there's a great deal of bearishness on the company's future in wireless baked into the shares, bearishness that may well overlook the company's strong IP position in system-on-a-chip technologies. While I would not be cavalier about the threat of competition from Qualcomm or Intel (Nasdaq:INTC), nor the risk of "home-grown" solutions from Samsung and/or Apple, I think a lot of the downside may already be in the market.

Just 2% long-term annual free cash flow growth would suggest that Broadcom shares should trade closer to $33 or $34, while I think a worst-case scenario would fall around $27 or $28 per share. There are certainly risks tied to shrinking market growth, shrinking margins, and increasing competition, and these are not shares for investors who don't like or tolerate risk. Even so, while I don't think its appropriate to approach Broadcom with a buy-and-forget mentality, I do believe the shares are too cheap below $28.

Disclosure – At the time of writing, the author owned no shares of companies mentioned in this article.

Popular Posts: Store Your Cash In These 3 Self-Storage REITsMore Dividend Growth Ahead From KMI Stock3 Pros, 3 Cons For TRP Stock & The Keystone XL Pipeline Recent Posts: The Sun Is Setting for Chinese Solar Stocks 4 Stocks to Buy to Hedge Against Higher Gas Prices Store Your Cash In These 3 Self-Storage REITs View All Posts

Popular Posts: Store Your Cash In These 3 Self-Storage REITsMore Dividend Growth Ahead From KMI Stock3 Pros, 3 Cons For TRP Stock & The Keystone XL Pipeline Recent Posts: The Sun Is Setting for Chinese Solar Stocks 4 Stocks to Buy to Hedge Against Higher Gas Prices Store Your Cash In These 3 Self-Storage REITs View All Posts  Source: Flickr

Source: Flickr  As one of the nation's largest independent downstream players, Valero (VLO) is in a prime position to profit from exporting refined petroleum products and rising gas prices. In fact, VLO has made sending gasoline and diesel overseas one of its main pillars of profit.

As one of the nation's largest independent downstream players, Valero (VLO) is in a prime position to profit from exporting refined petroleum products and rising gas prices. In fact, VLO has made sending gasoline and diesel overseas one of its main pillars of profit. As if ConocoPhillips (COP) spinoff Phillips 66 (PSX) needed any more positives. PSX is already becoming a major player in liquefied petroleum gas (LPG) and propane exports. Meanwhile, it's a major midstream and natural gas processor as well. All of these refining activities are boosting the firm's bottom line.

As if ConocoPhillips (COP) spinoff Phillips 66 (PSX) needed any more positives. PSX is already becoming a major player in liquefied petroleum gas (LPG) and propane exports. Meanwhile, it's a major midstream and natural gas processor as well. All of these refining activities are boosting the firm's bottom line. It shouldn't come as a shock that midstream giant Enterprise Products Partners, LP (EPD) is one of the best ways to play rising gas prices. When you're one of the largest midstream master limited partnerships (MLPs) in the country, you have your hands in a variety of different energy commodities. That includes pipelines that transport refined gasoline to export terminals.

It shouldn't come as a shock that midstream giant Enterprise Products Partners, LP (EPD) is one of the best ways to play rising gas prices. When you're one of the largest midstream master limited partnerships (MLPs) in the country, you have your hands in a variety of different energy commodities. That includes pipelines that transport refined gasoline to export terminals. One of the best ways to hedge against rising gas prices is to directly bet on that happening. The exchange-traded fund boom has made it easy for anyone with a brokerage account to hedge their gasoline consumption.

One of the best ways to hedge against rising gas prices is to directly bet on that happening. The exchange-traded fund boom has made it easy for anyone with a brokerage account to hedge their gasoline consumption.

The second rule is that only the uninformed focus exclusively on if the company beat or missed earnings expectations. Earnings results are just that, results that report what happened BEFORE. But the market focuses on what WILL happen. Big-money Wall Street fund managers -- the whales that move a stock price -- review last quarter's results only up to the point the data aids in predicting future expectations. While many are satisfied if Under Armour, Amazon and Microsoft outperform their previous quarter, fund managers closely scrutinize margin trends, forward guidance, growth rates (or lack thereof), competitive influences, management changes, cash flow, dilution and other factors. They are painting a picture of the next quarter, the next year and beyond. The third rule is that one quarter doesn't matter. That's a hard one for many to understand in the heat of battle. Patterns can't be found in sample sizes of one. Fund managers plug a given company's results into spreadsheets and compare the results with previous quarters to find hidden patterns and trends.

The second rule is that only the uninformed focus exclusively on if the company beat or missed earnings expectations. Earnings results are just that, results that report what happened BEFORE. But the market focuses on what WILL happen. Big-money Wall Street fund managers -- the whales that move a stock price -- review last quarter's results only up to the point the data aids in predicting future expectations. While many are satisfied if Under Armour, Amazon and Microsoft outperform their previous quarter, fund managers closely scrutinize margin trends, forward guidance, growth rates (or lack thereof), competitive influences, management changes, cash flow, dilution and other factors. They are painting a picture of the next quarter, the next year and beyond. The third rule is that one quarter doesn't matter. That's a hard one for many to understand in the heat of battle. Patterns can't be found in sample sizes of one. Fund managers plug a given company's results into spreadsheets and compare the results with previous quarters to find hidden patterns and trends.

Mario Tama/Getty Images

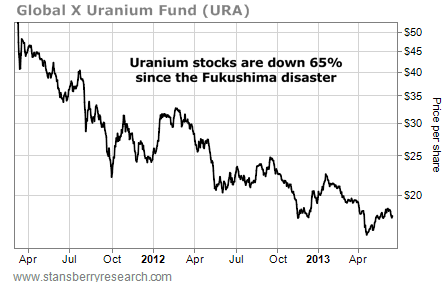

Mario Tama/Getty Images  Today, most uranium producers are losing money. Marin says African uranium producers need prices to hit $75 per pound for them to make money. For most of Europe, it's over $65 per pound. And in the U.S., you need between $45 and $50. The current spot price of uranium is just $40 a pound. And as Marin put it, if uranium prices don't head higher from here, most companies will have to turn the lights off. Then Marin explained another shocking statistic... "If you want to get delivery of uranium five years out, you have to pay $68 [per pound] today." Marin's talking about the "futures" market. Sectors like trucking, airlines, and utilities use the futures market to lock in prices for years down the road. They do that so they don't have to worry about big fluctuations in energy prices. In other words... right now, companies that need to secure uranium supplies for the future are willing to pay $68 a pound – a 70% premium to spot prices – because they believe prices are going to be even higher than that five years from now. If that was the setup in gold or silver today, people would be buying hand over fist. But that's the great thing about buying uranium stocks here. That is the situation... and nobody's paying any attention. I've never seen this setup before in my investing lifetime. Cameco (NYSE: CCJ) is the biggest uranium producer in the world and a good trade on a recovery for the sector. However, if uranium producers do rebound from these depressed levels, the biggest returns will come from the more speculative names. Now, I don't suggest rushing out and buying every small uranium stock you can get your hands on. You need to do your research. And the No. 1 priority in considering a uranium investment is the people who run it. "Do you trust them? Are they focused on the company... or do they have five other companies?" Marin asks. "If there's a management team that has no money in the company, they're paid a high salary, they do consulting for other companies, and the only interest they have in this company is their salary and their options... Do you want to invest in that? No." That factor takes away a huge percentage of small uranium miners. But do your research. If you invest in the right companies, you could be sitting on big gains a few years from now when the rest of the market finally catches on. Good investing, Frank Curzio

Today, most uranium producers are losing money. Marin says African uranium producers need prices to hit $75 per pound for them to make money. For most of Europe, it's over $65 per pound. And in the U.S., you need between $45 and $50. The current spot price of uranium is just $40 a pound. And as Marin put it, if uranium prices don't head higher from here, most companies will have to turn the lights off. Then Marin explained another shocking statistic... "If you want to get delivery of uranium five years out, you have to pay $68 [per pound] today." Marin's talking about the "futures" market. Sectors like trucking, airlines, and utilities use the futures market to lock in prices for years down the road. They do that so they don't have to worry about big fluctuations in energy prices. In other words... right now, companies that need to secure uranium supplies for the future are willing to pay $68 a pound – a 70% premium to spot prices – because they believe prices are going to be even higher than that five years from now. If that was the setup in gold or silver today, people would be buying hand over fist. But that's the great thing about buying uranium stocks here. That is the situation... and nobody's paying any attention. I've never seen this setup before in my investing lifetime. Cameco (NYSE: CCJ) is the biggest uranium producer in the world and a good trade on a recovery for the sector. However, if uranium producers do rebound from these depressed levels, the biggest returns will come from the more speculative names. Now, I don't suggest rushing out and buying every small uranium stock you can get your hands on. You need to do your research. And the No. 1 priority in considering a uranium investment is the people who run it. "Do you trust them? Are they focused on the company... or do they have five other companies?" Marin asks. "If there's a management team that has no money in the company, they're paid a high salary, they do consulting for other companies, and the only interest they have in this company is their salary and their options... Do you want to invest in that? No." That factor takes away a huge percentage of small uranium miners. But do your research. If you invest in the right companies, you could be sitting on big gains a few years from now when the rest of the market finally catches on. Good investing, Frank Curzio

Annalisa Linder A glorious Saturday afternoon, and Sears is virtually empty. Merchandise is all jumbled; aisles are blocked; it looks dispirited. After a spate of photo stories on the disarray at Sears, I wanted to look for myself. The sadder side of Sears, indeed. J.C. Penney (JCP) and Macy's (M) in the same mall in suburban Maryland were busier, neater and drawing younger customers.

Annalisa Linder A glorious Saturday afternoon, and Sears is virtually empty. Merchandise is all jumbled; aisles are blocked; it looks dispirited. After a spate of photo stories on the disarray at Sears, I wanted to look for myself. The sadder side of Sears, indeed. J.C. Penney (JCP) and Macy's (M) in the same mall in suburban Maryland were busier, neater and drawing younger customers.  Annalisa Linder If you remember the slogan, "the softer side of Sears," then you're the typical Sears age demographic, and if you never heard it, you are the younger shopper it desires but can't attract. Sears Holdings' (SHLD) sales have declined for years as it loses customers to Kohl's (KSS) and J.C. Penney and younger customers throng to Macy's. Most mall anchor stores are struggling. A recent Piper Jaffray survey found that teens aren't hanging out at the mall anymore and prefer a social "experience," preferably at a restaurant. Sears and Sears Holdings' Kmart stores have been hit particularly hard. CEO Eddie Lampert noted on the most recent earnings call that shoppers only visit three stores per mall trip now, compared to five in 2007. The Sadder Side of Sears

Annalisa Linder If you remember the slogan, "the softer side of Sears," then you're the typical Sears age demographic, and if you never heard it, you are the younger shopper it desires but can't attract. Sears Holdings' (SHLD) sales have declined for years as it loses customers to Kohl's (KSS) and J.C. Penney and younger customers throng to Macy's. Most mall anchor stores are struggling. A recent Piper Jaffray survey found that teens aren't hanging out at the mall anymore and prefer a social "experience," preferably at a restaurant. Sears and Sears Holdings' Kmart stores have been hit particularly hard. CEO Eddie Lampert noted on the most recent earnings call that shoppers only visit three stores per mall trip now, compared to five in 2007. The Sadder Side of Sears

NEW YORK (CNNMoney) Millions of people are filing their taxes just as governments grapple with Heartbleed, the worst privacy-killing Internet bug ever.

NEW YORK (CNNMoney) Millions of people are filing their taxes just as governments grapple with Heartbleed, the worst privacy-killing Internet bug ever.  Heartbleed: 'Secure' internet wasn't safe

Heartbleed: 'Secure' internet wasn't safe